Product

Product overview

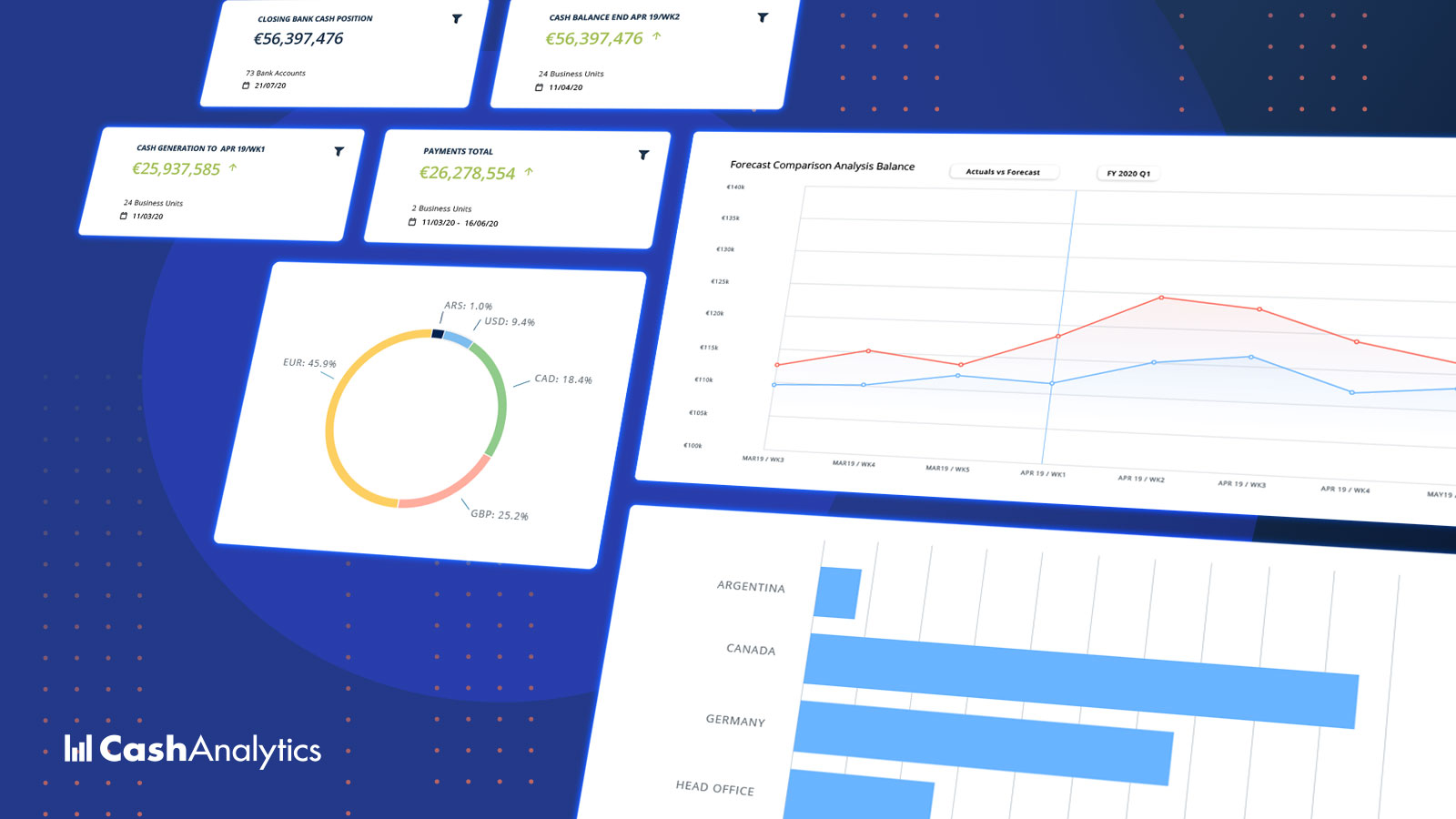

Cash Flow Forecasting

Bank Account Reporting

AP and AR Analytics

Use Cases

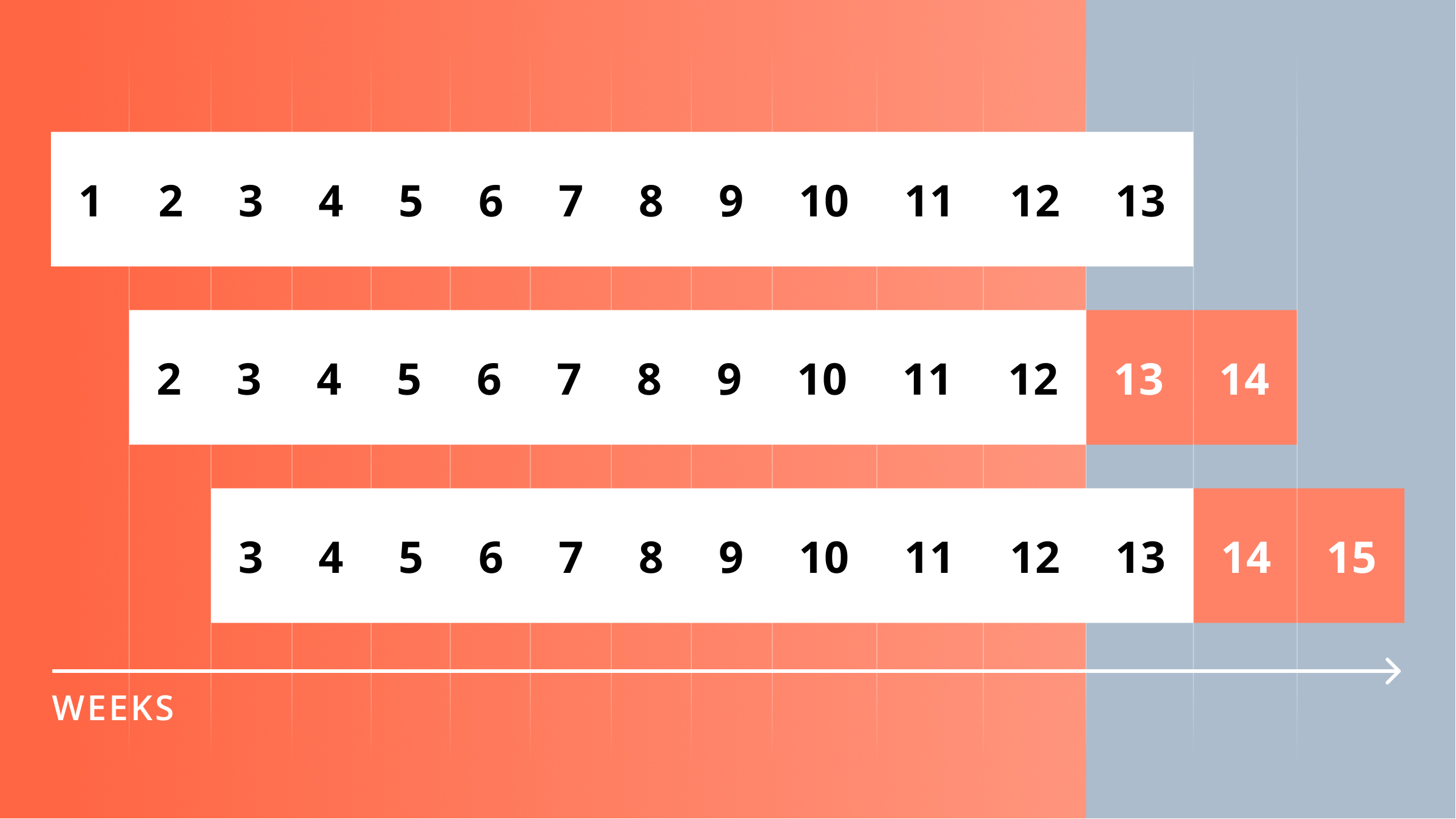

13 Week Cash Flow Forecasting

Multi-Location Forecasting

Liquidity Management

Bank Connectivity & Reporting

Working Capital Analysis

Accounts Receivable Forecasting

Customers

Pricing

Company

About us

Technology and Security

Resources

Blog

Contact Us

Book a demo

Book a demo

Book a demo

Software & Tools

Cash Flow Forecasting Software

Cash Flow Forecasting Tool

Driver Based Forecasting Software

Corporate Bank Reporting

Process & Setup

Cash Flow Forecasting Process

Cash Forecasting Automation

Cash Flow Forecasting Template

13 Week Cash Flow

Daily Cash Flow

Monthly Cash Flow Forecast

Covenant Forecasting

Differences between Direct and Indirect Cash Forecasting

Accuracy & Analytics

How to increase accounts receivable forecasting accuracy

In-depth Reporting and Analytics

Cash forecasting data visualisations

Popular Articles

Critical Activities Supported by your Cash Flow Forecast

5 Reasons to Automate your Cash Forecasting in 2023

How High Interest Rates and Inflation Eat your Cash Flow

Cash Forecasting Visibility

Cash Flow KPI

Working Capital Management

Cash Conversion Cycle

Cash Flow Liquidity

Cash Flow Dashboard

Rolling Cash Flow Forecast

Cash Flow Projection

Liquidity Risk Management

Cash and Liquidity Management

Liquidity Management Planning

Cash Flow Forecasting

Cash Forecasting Model

Cashflow Forecasting Best Practice

Cash Reporting Platform

Customer Stories

Kingfisher

NCC Group

Jost

Peak Toolworks

Stella McCartney

Excellence Logging

Rubix

Sulzer

SSP Group

CEVA Logistics

Latest

Latest

Cash Flow Dashboard

Cash Flow Metrics

Cash Forecasting

Cash Management

Customers

Liquidity

Liquidity Risk Management

Technology

Webinar

Working Capital Management

Working Capital Monitor

Cash Management

How to Evaluate and Improve Working Capital Management

Cash Forecasting

What is a Cash Conversion Cycle? How to Shorten Your Cash Conversion Cycle

Cash Forecasting

How Does a Cash Flow Liquidity Forecast Help in a Time of Uncertainty

Cash Flow Dashboard

How to choose the right metrics for your cash flow dashboard

Cash Forecasting

Why All Our Clients Use Rolling Cash Flow Forecast

Cash Forecasting

Why Companies Automate Cash Forecasting

Cash Flow Metrics

The Key Cash Flow Metrics All Large Companies Should Track

Liquidity

Governance: The Future of Liquidity Risk Management

Cash Forecasting

How the Rise of Private Equity helped Popularize the 13-week Cash Flow Forecast

Cash Forecasting

How to set up a best practice 13-week cash flow forecast

Cash Forecasting

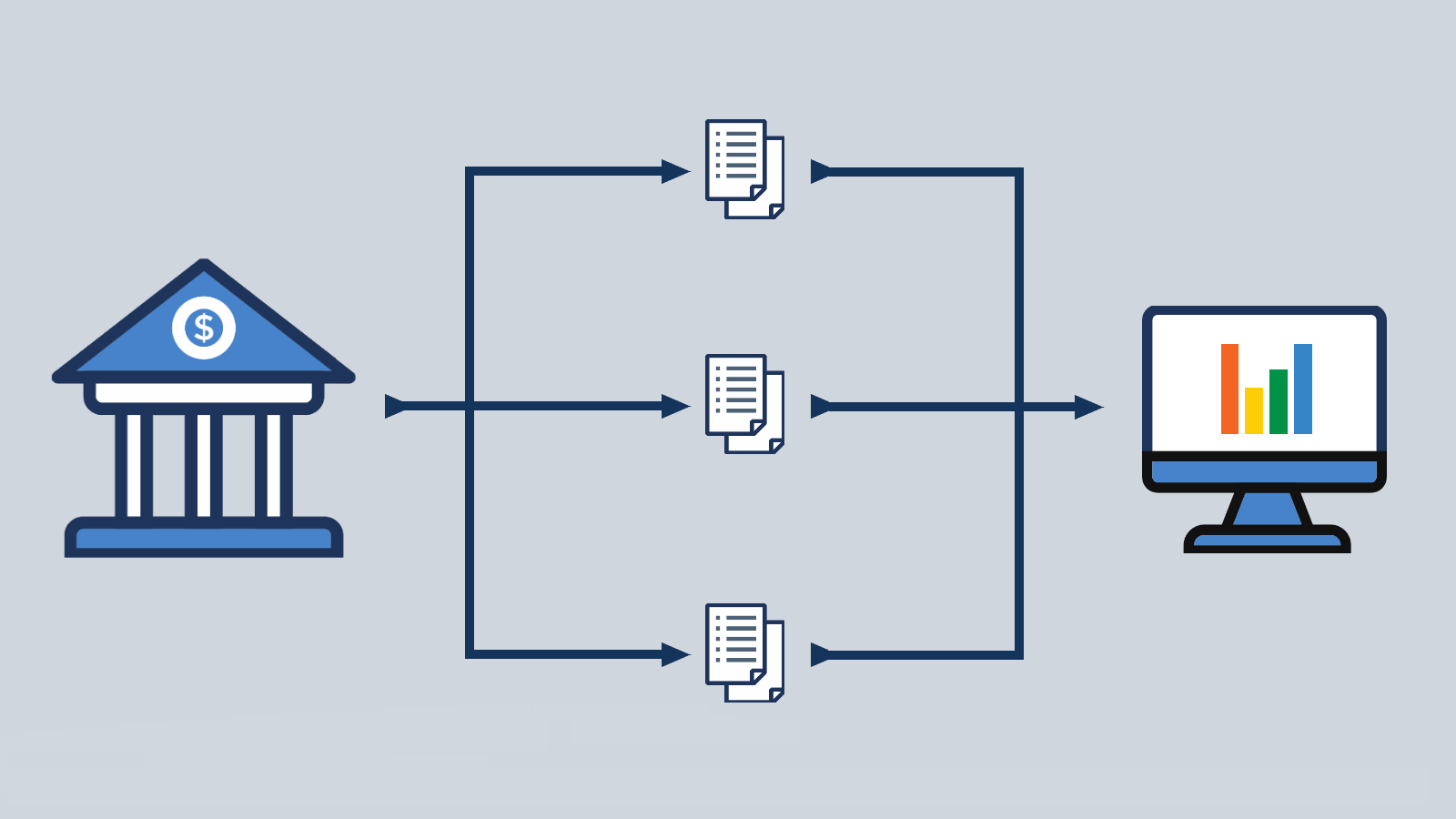

How electronic bank statements enable automated bank reporting

Cash Forecasting

Data visualisation: accelerating the rise of finance and treasury

Page 3 of 6

Previous

1

2

3

4

5

Next

Next

Last »